Market Overview

This week, the storage market faced severe shortages, with a clear upward price trend across the board. “Do you have stock?” has become a hot topic in the industry.

Market activity surged, with increased trading volume and rising prices driven by earlier production cuts from suppliers and China’s consumer electronics subsidy policies. Optimism prevails as industry players anticipate price recoveries starting in Q2. Improving supply-demand dynamics and growing AI device demand are further fueling market recovery.

Key Developments

Samsung Electronics: Q1 shipments are projected to decline, reducing available inventory.

NAND: Prices began rising in January.

DRAM: Prices stabilized for three consecutive months.

Market Sentiment: Prices have bottomed out, but supplier strategies will dictate future trends.

Flash Wafers: Demand improved, trading surged, and prices climbed.

Flash Insights Analysis

The market shows signs of recovery: prices are trending upward, inventories are depleting, and shortages are widespread. Cautious optimism is advised, with close monitoring of supplier actions.

SSD Market

Prices continued to rise this week, driven by scarce low-cost resources and higher production costs. Most low-capacity products (128/256/512GB) are unquoted, while high-capacity prices surged over 5%. Module factories report component shortages until late month. Brand and enterprise segments remain stable but may follow the upward trend. This rally could persist, depending on supplier responses.

SSD Price Trends

NVMe 3.0: All capacities up 1-3%.

NVMe 4.0: All capacities up ~1% (except 480GB, flat).

SATA 3.0: All capacities up 3-12%.

DRAM Market

Prices saw a slight rebound, injecting optimism despite lingering caution.

The 2025 memory market remains unpredictable. While some analysts expected continuous price drops, recent supply chain adjustments by manufacturers have created mixed signals.

Kingston’s Market Strategy

With 40 years in the industry, Kingston shares these insights:

NAND prices: Short-term fluctuations expected

DDR4 stability: Production cuts maintain pricing

DDR5 adoption: Dependent on new tech adoption

“We’re seeing DDR5’s future tied to AI devices and premium PCs. Until then, we’ll keep flexible strategies.”

Shenzhen Market Report

Local traders in Huaqiangbei electronics market observe:

Product

Price Change

Inventory Level

DDR4 Memory

-1.5% weekly

45 days supply

1TB SSD

+2.8%

Low stock

“The SSD price jump started when factories held back stock after Lunar New Year,” explains a local wholesaler.

Key Market Signals

NVMe 4.0 drives spike (+14%)

DDR5 adoption slower than expected

AI infrastructure driving enterprise demand

Industry watchers suggest: “Monitor daily spot prices and diversify suppliers.”

Kioxia Corporation and Western Digital’s SanDisk have jointly developed the 10th generation BiCS 3D NAND flash memory, achieving world-leading specifications in:

Stacking layers (332 layers)

Storage density (36.4Gb/mm²)

Interface speed (4800MT/s)

Technological Innovations

Adopting CBA (CMOS Bonded Array) wafer bonding technology inspired by Yangtze Memory’s Xtacking architecture, the new design separates CMOS control circuits from memory arrays for optimized performance.

3D NAND flash memory Layer Stack Comparison

Kioxia: 332 layers (+38% vs 8th gen)

SK Hynix: 321 layers

Samsung: 290 layers

Micron: 276 layers

Global Storage Evolution: 332-Layer 3D NAND flash memory Milestones vs Quantum Storage Breakthroughs (2023-2030)

Timeline

Technology Area

Key Milestone

Technical Specifications

Major Players

Future Targets

2023 Q3

3D NAND Stacking

World’s first 332-layer flash

36.4Gb/mm² density

4800MT/s speed

Kioxia/WD

1000-layer by 2027

2024 (Projected)

Controller Technology

64-channel UltraQLC controller

64 NAND channels

Hardware acceleration

SanDisk

256TB SSD by 2025

2025 (Roadmap)

QLC Storage

2Tb NAND implementation

128TB SSD capacity

Adaptive power management

Western Digital

512TB SSD by 2027

2026 (Research)

Quantum Storage

Crystal defect utilization

1mm³ crystal storage

TB-scale capacity

UChicago PME

Commercialization research

2030 (Target)

Petabyte Storage

UltraQLC full implementation

1PB SSD capacity

64+ channel support

Industry Consortium

Exabyte-scale solutions

Power Efficiency Advancements

The new PI-LTT (Precision Input – Low Temperature Transfer) technology reduces:

Input power consumption: 10% reduction

Output power consumption: 34% reduction

Roadmap to Exabyte Storage

SanDisk’s UltraQLC platform combines:

64-channel custom controller

BICS 8 QLC 3D NAND

Adaptive power management

Projected capacities:

2025: 256TB

2027: 512TB

2030: 1PB

Revolutionary Crystal Storage Technology

University of Chicago researchers achieved terabyte-scale storage in 1mm³ crystals using:

Praseodymium-doped yttrium oxide substrates

UV laser charge trapping

Quantum-inspired binary encoding

Key breakthrough: Utilizing crystal defects as binary storage units with:

Charged defects = 1

Neutral defects = 0

Global NAND Demand Drivers

Application

2025 Demand (Exabytes)

2030 Projection

Growth Rate

AI Training

180 EB

1,200 EB

55% CAGR

Smartphones

650 EB

950 EB

8% CAGR

Data Centers

420 EB

1,800 EB

34% CAGR

EV Storage

30 EB

280 EB

65% CAGR

Source: TrendForce & Gartner (Q2 2024 Data)

Patent Control Landscape

Company

Hybrid Bonding Patents

Key Markets

Yangtze Memory

1,240+

China (80%), Global OEMs

Samsung

890

Korea, USA, EU

SK Hynix

670

Enterprise Storage

Western Digital

550

Cloud Providers

2026 Price War Forecast

Scenario

2TB SSD Price

YMTC Impact

Base Case

$75

30% market share

Tech Breakthrough

$65

45% market share

Trade War Escalation

$95

15% export limit

*Assumes 5% annual density improvement

“YMTC’s Xtacking 3.0 could capture 25% of global NAND capacity by 2028, fundamentally reshaping the $80B memory market dynamics.”

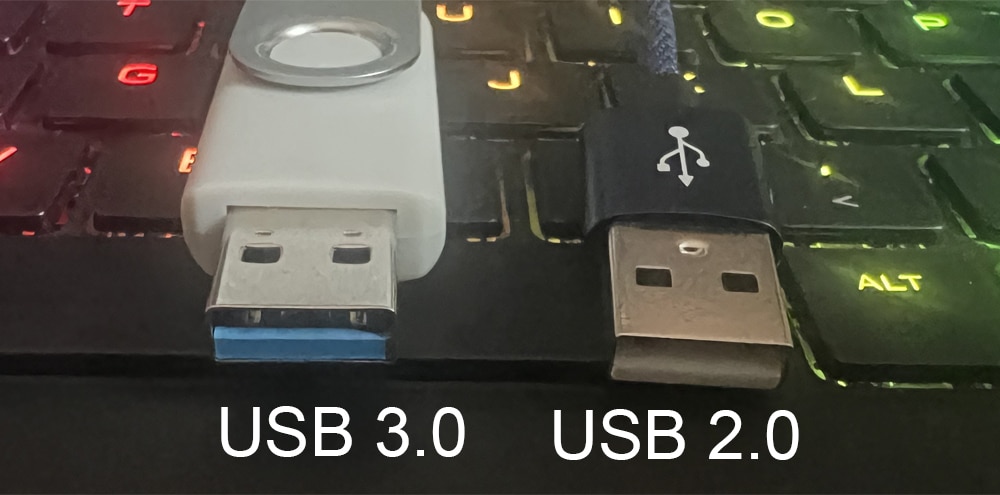

Released in August 2014, the USB Type-C connector, measuring a sleek 8.4mm x 2.6mm, is slightly larger than USB 2.0 Micro-B but offers universal compatibility. This versatile reversible interface supports:

15W base charging with USB Power Delivery (USB PD) extension up to 100W

10 Gbps data transfer (USB 3.1 Gen 2) with future-proof scalability for USB4 speeds

Seamless integration with smartphones, tablets, and ultra-thin laptops

USB Type-C Specifications: USB-C 2.0, 3.0, and 4.0

USB Type-C 2.0

Speed: Up to 480 Mbps data transfer (same as USB 2.0)

Power Delivery: Supports up to 1.5A and 7.5W power

Compatibility: Backward compatible with USB 2.0 devices

USB Type-C 3.0 (USB 3.1 Gen 1)

Speed: Up to 5 Gbps data transfer

Power Delivery: Supports up to 3A and 15W power

Compatibility: Backward compatible with USB 2.0 devices

USB Type-C 3.1 Gen 2

Speed: Up to 10 Gbps data transfer

Power Delivery: Supports up to 5A and 30W power

Compatibility: Backward compatible with USB 3.0 and USB 2.0 devices

USB Type-C 4.0

Speed: Up to 40 Gbps data transfer, rivaling Thunderbolt 3 speeds

Power Delivery: Supports up to 100W (20V at 5A) power

Compatibility: Backward compatible with all previous USB standards

Advantages of USB 3.0

Data Transfer Speed

High-Speed Transfer

USB 3.0 offers a theoretical data transfer speed of up to 5 Gbps (Gigabits per second). This is a significant improvement over USB 2.0, which has a theoretical speed of 480 Mbps (Megabits per second). In practical applications, USB 3.0 enables much faster file transfers.

For example, when transferring a large high-definition video file (e.g., 5GB), USB 2.0 may take several minutes or even over ten minutes, while USB 3.0 can complete the transfer in just tens of seconds to one or two minutes.

Consistent Transfer Speed

USB 3.0 can maintain a relatively stable transfer speed. When continuously transferring multiple files or performing block transfers of large files, USB 3.0 is less likely to experience significant speed fluctuations. This is highly beneficial for scenarios that require long-duration and large-volume data transfers, such as backing up data to an external hard drive.

Power Supply Capability

Higher Power Output

USB 3.0 can provide up to 4.5W of power (typically achieved with a 5V voltage and 0.9A current). This is a substantial increase compared to USB 2.0’s maximum power output of 2.5W (5V/0.5A). The higher power output allows USB 3.0 to charge a wider range of devices.

For instance, it can directly charge devices like some higher-power portable hard drives or small Bluetooth headsets that may require more power than what USB 2.0 can provide.

Compatibility

Backward Compatibility

USB 3.0 is fully compatible with USB 2.0 devices. This means that when you connect a USB 2.0 device (such as an old USB flash drive or mouse) to a USB 3.0 port, the device will still function properly. Although the transfer speed will be limited to the USB 2.0 standard, the device remains usable.

Hardware Compatibility

In terms of hardware design, the USB 3.0 interface is similar in appearance to the USB 2.0 interface. Moreover, when a motherboard or device is equipped with both USB 2.0 and USB 3.0 ports, they can work well together without causing hardware conflicts.

Other Advantages

Support for More Device Types

Due to its improved speed and power capabilities, USB 3.0 can better support emerging device types. For example, high-speed network cameras, high-resolution digital cameras, and other devices that require rapid data transfer to ensure image and video quality, as well as those that need a certain amount of power to operate normally, can benefit from USB 3.0.

Enhanced User Experience

In daily use, tasks such as copying files from a portable hard drive to a computer quickly, storing and retrieving data using high-speed USB flash drives, etc., become more efficient. Additionally, when connecting multiple USB devices simultaneously, USB 3.0 can better coordinate the work between them, reducing interference between devices.

Comparison of USB Type-C Rates

USB Standard

Data Transfer Speed

Power Delivery

Compatibility

USB – C 2.0

480 Mbps

7.5W

Backward compatible with USB 2.0

USB – C 3.0

5 Gbps

15W

Backward compatible with USB 2.0

USB – C 3.1 Gen 2

10 Gbps

30W

Backward compatible with USB 3.0 and 2.0

USB – C 4.0

40 Gbps

100W

Backward compatible with all USB standards

4 Key Advantages of USB Type-C Technology

1. Compact Design

Matches the footprint of legacy USB 2.0 Micro-B ports while enabling advanced functionality.

2. High – Power Charging

Delivers up to 100W via USB PD — enough to power premium laptops and monitors.

3. Future – Ready Architecture

Supports evolving standards including USB4, Thunderbolt™ 3/4, and DisplayPort Alt Mode.

4. Reversible Usability

Eliminates orientation frustration with dual – sided pluggability like Apple’s Lightning connector.

USB Type-C Authentication Protocol: Security Features

The USB – IF’s 2019 certification program implements cryptographic validation to prevent uncertified accessories from connecting. Core components include:

Device/Cable/Charger authentication via USB PD communication

128 – bit encryption with FIPS – compliant algorithms

Globally recognized certificate formats and digital signatures

Customizable security policies for OEMs

The Evolution of USB Type-C: Market Impact & Predictions

Since the EU’s 2017 charger standardization mandate, USB – C adoption has surged by 62% annually (ABI Research). Key developments:

Mobile Unification: Phased out Micro-B ports in flagship Android/iOS devices

Cross – Device Compatibility: Single – cable solutions for data, 8K video, and 240W charging (USB PD 3.1)

IoT Expansion: Emerging as default interface for AR/VR headsets and industrial equipment

Analysts project USB – C will dominate 98% of consumer electronics by 2025, replacing HDMI, 3.5mm audio, and proprietary charging ports.

Friends who often replace graphics cards know that it’s hard to deal with the old ones after upgrading. Throwing them in the trash takes up space, and selling them second-hand is painful. You might not know that a graphics card that’s outdated on a desktop can give a laptop a significant performance boost when installed.

How can you put a graphics card in a laptop? This brings us to the laptop graphics card docking station, a magical device. My model is the Planit PL-LINK S-1, which allows you to connect a desktop graphics card to your laptop. When you get home, just connect your laptop, and the performance is instantly improved. When you’re on the go, unplug and you’re ready to leave.

This device is mainly simple and affordable. Inside the packaging, you’ll find, besides the docking station, a Thunderbolt cable, a screwdriver, and matching screws, as well as a fixing bracket.

The docking station has an open design with a power interface and a graphics card interface on the front. Notice that there’s a cover over the power interface that can be removed to accommodate an M.2 2280 solid-state drive, which seems to be very necessary for expanding the storage of Apple laptops.

Although Windows systems don’t need it, you can’t be without it. On the side, there’s a power button, a network interface, and two Thunderbolt 3 ports. The Thunderbolt 3 port with the small computer supports 60W, while the other Thunderbolt 3 only supports up to 15W. If you have a thin and light laptop, you basically don’t need to consider additional power supply; this docking station can provide power.

The product assembly is very simple. Plug in the idle graphics card, place the power supply, and secure it with screws. There’s also a small bracket between the graphics card and the power supply, which holds the graphics card in place.

Connect the power supply and graphics card, and you’ll see that this open work platform looks very cool, with a full industrial cyberpunk style.

When you power up, the power supply and graphics card fans spin very fast. Once connected to the computer, the fan speed immediately slows down.

After connecting to the computer, the computer immediately recognizes the docking station and the graphics card. The docking station is plug-and-play, but the graphics card requires the installation of the latest drivers. Using a detection tool to check the laptop, it has successfully installed the graphics card and drivers, and it is also recognized as the primary graphics card by default. Running a benchmark with Master Lu, it easily breaks through 1.28 million points, with a significant improvement in graphics performance. Of course, this is greatly related to the graphics card. I’m using an RTX 2070S here, which just makes up for the shortcomings. This docking station can support up to RTX 40 series graphics cards.

Now, let’s get down to work. I’m in the self-media industry, and I often work with photo editing, video editing, and live streaming. Don’t underestimate these tasks; they require a lot of CPU and GPU performance. When using a laptop, the preview starts to lag when there are a few more effects during editing. But with the external graphics card, previewing with six effects is also very smooth. During the editing process, reversing video is very GPU-intensive. Without a dedicated graphics card, reversing video is the most troublesome, as it’s super slow. Now, with a dedicated graphics card, reversing video is very fast. A 30-second original video is reversed in just a few seconds, and the efficiency has greatly improved.

When reversing, I specifically checked the Task Manager, and the GPU usage was already over 90%. No wonder it was so slow without dedicated graphics card acceleration.

Next up is the live streaming experience. I use OBS for dual-camera live streaming here, and I also record the live content for later editing and republishing as videos. I tried it with a laptop before; it could handle dual-camera streaming, but adding recording caused significant frame drops, and it couldn’t maintain 25 frames for more than a few minutes. Now, with a dedicated graphics card, I’m not worried anymore; dual-camera live streaming plus recording is very stable.

I glanced at the Task Manager, and the GPU was utilized at over 90% throughout the process, but the noise from the power supply fan and the graphics card fan was very low, so much so that it wouldn’t even be picked up by the microphone. The fan control on the docking station is quite good, but the only thing I worry about is the dust issue with the open structure; should I DIY an acrylic transparent cover?

The processors in thin and light laptops are all hyped up, but the integrated graphics are what let them down. My laptop used to only run “CS:GO” at over 100 frames, and I knew my laptop’s capabilities, so I didn’t have high expectations. But now it’s different; I want to compete on the battlefield too. After connecting a graphics card to the laptop, the FPS easily reaches over 300 frames, smooth and silky.

Even games like “PlayerUnknown’s Battlegrounds” (PUBG), which I didn’t dare to play before, are now within reach. Before the docking station, my laptop could only manage 40-50 frames, with stuttering every jump and step, making it really unenjoyable. Now, I have a smooth experience with 140 frames.

No wonder I couldn’t play PUBG on my laptop before; even in the lobby doing nothing, the GPU usage reached 70%, which the laptop’s integrated graphics couldn’t handle.

I’ve calculated that this docking station can deliver about 90% of the graphics card’s performance, compared to the same version of Master Lu’s benchmark scores on a PC and a laptop. After all, this docking station is only a few hundred dollars; you can’t expect it to give 100%, right? The performance of a graphics card docking station mainly depends on the graphics card used. A high-end graphics card docking station might deliver about 95% of the graphics card’s performance, but the price difference is too high, and the extra money spent is really unnecessary.

After using this docking station for a while, I’ve found it to be really good, especially for those who already have a power supply and a graphics card. Spending a little money gives your laptop the performance of a desktop computer, which is quite cost-effective.

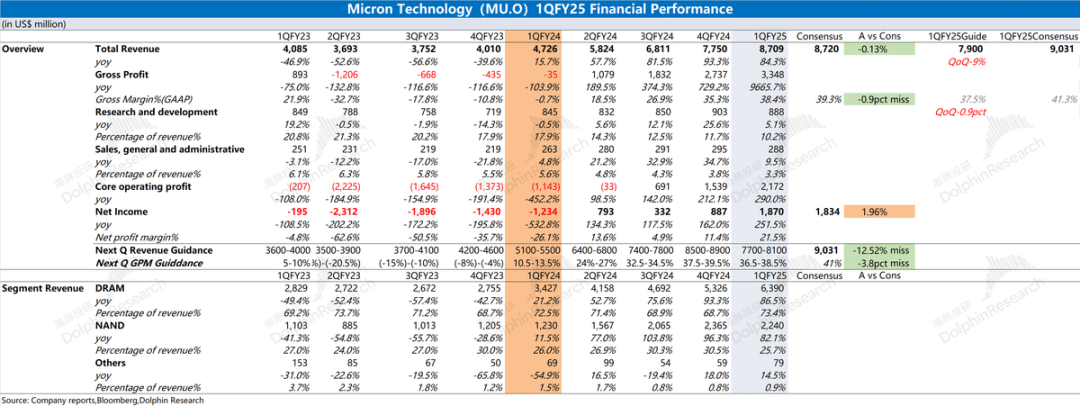

Micron (MU.O) released its financial results for the first quarter of the fiscal year 2025 (ending November 2024) after the US stock market closed on the morning of December 19, 2024, Beijing time. The key points are as follows:

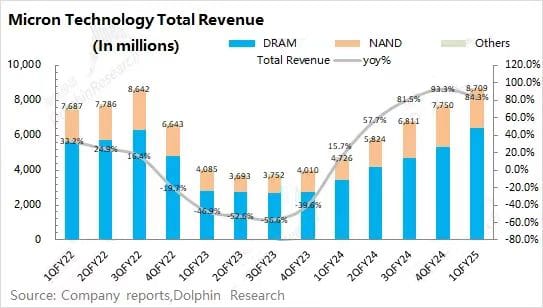

Overall Performance: Revenue met expectations, but gross margin faced challenges. Micron’s total revenue for the first quarter of the fiscal year 2025 was $8.7 billion, an increase of 84.3% year-over-year, in line with market expectations ($8.72 billion). The revenue continued to rebound, driven by the company’s DRAM business growth. Micron achieved a net profit of $1.87 billion in the first quarter of the fiscal year 2025, with profits continuing to improve. Driven by the volume of HBM and the rise in storage product prices, both the company’s revenue and gross margin saw significant improvements, leading to a noticeable improvement in the company’s bottom line.

Business Segment Performance: HBM is the main driver of performance. DRAM and NAND account for 99% of the company’s revenue, and HBM was the main driver of performance growth this quarter. Specifically, while both DRAM and NAND businesses saw significant year-over-year growth, there was a clear divergence on a quarter-over-quarter basis. DRAM business still grew by 20% quarter-over-quarter, while NAND business declined by 5%. This was mainly because DRAM continued to grow under the impetus of HBM, while the weakness in demand in traditional areas directly led to a quarter-over-quarter decline in NAND business.

Outlook for the Next Quarter: Revenue for the second quarter of the fiscal year 2025 is expected to be between $7.9 billion and $8.1 billion (a quarter-over-quarter decline of 9%), below the market consensus expectation ($9 billion); the quarterly gross margin (GAAP) is expected to be between 36.5% and 38.5%, which is also a quarter-over-quarter decline and below the market consensus expectation (41.3%).

Overall view: The financial report for this quarter was somewhat satisfactory, but the guidance for the next quarter was disappointing. Micron’s revenue and gross margin continued to rebound this quarter, but the gross margin performance did not meet market expectations. Although HBM is still contributing to the company’s growth, the company was affected by traditional downstream markets such as mobile phones this quarter, leading to a decline in prices for some storage products, which in turn affected the gross margin performance. Looking at the business segments, the company’s DRAM business still saw a 20% quarter-over-quarter growth this quarter. Driven by HBM, the DRAM business continued to show an increase in both volume and price; however, the company’s NAND business declined by 5% quarter-over-quarter. This was mainly due to the impact of inventory adjustments in downstream sectors such as mobile phones, automobiles, and industry, with a slight quarter-over-quarter decline in both shipment volume and average price of related storage products. Compared to this quarter’s financial report, the company’s outlook for the next quarter is indeed “poor.” It not only interrupted the company’s continuous growth in revenue for seven consecutive quarters but also saw a decline of nearly $800 million quarter-over-quarter, and the gross margin may also decline quarter-over-quarter. This will undoubtedly add more concerns to the market: 1) Has the company’s current storage upcycle ended? 2) Is the company’s HBM business growth hindered? This directly led to a 16% decline in the company’s stock price after the market closed.

Considering the industry and the company’s operating conditions, the decline in revenue for the next quarter is still mainly affected by sectors such as mobile phones and automobiles. From several perspectives: 1) The traditional areas are still in the inventory adjustment phase, and the company expects to gradually stabilize after the second half of the fiscal year 2025 (after March 2025 in the calendar year); 2) The company has further increased its total market size expectation for HBM next year to $30 billion (originally expected to be $25 billion), which shows the company’s confidence in the HBM business; 3) Recent rumors about NVIDIA adjusting the shipment structure of B200 and B300 will also affect the rhythm of Micron’s HBM to some extent. Overall, Micron’s current business includes both traditional storage demand and AI-related demands such as HBM. The company’s current performance is still mainly affected by traditional businesses, and the current downturn in traditional areas will directly affect the company’s subsequent business. As for the growth-oriented HBM business that the market is concerned about, although the current revenue share is still less than 10%, the company’s growth expectation for next year continues to be revised upwards. Therefore, the company’s performance will be under pressure in the first half of the fiscal year 2025, and with the destocking of downstream and the volume of HBM, the company’s performance is expected to see a significant improvement again in the second half of the year.

I. Overall Performance: Revenue meets expectations, but gross margin faces obstacles

1.1 Revenue

Micron’s total revenue for the first quarter of the fiscal year 2025 was $8.71 billion, a year-over-year increase of 84.3%, in line with market expectations ($8.72 billion). The revenue rebounded year-over-year, mainly driven by the price increase of the company’s storage products, with the average selling price of the company’s DRAM and NAND products both increasing by more than 60% year-over-year.

On a quarter-over-quarter basis, the company grew by 12.4%. Among them, the DRAM business still saw a 20% quarter-over-quarter growth this quarter, driven by HBM demand, while NAND saw a 5% quarter-over-quarter decline, mainly due to the impact of downstream inventory adjustments in the mobile phone, automotive, and industrial sectors.

1.2 Gross Margin

Micron achieved a gross profit of $3.348 billion in the first quarter of the fiscal year 2025, and the company’s quarterly gross profit continued to rebound. The company’s gross margin for this quarter was 38.4%, lower than market expectations (39.3%). The increase in gross margin was mainly due to the rise in the average price of DRAM products and their proportion, but the weakness in some downstream sectors affected the extent of the rebound in gross margin. Although the company’s current inventory is $8.705 billion, a quarter-over-quarter decline of 1.9%. With the recovery in sales and the destocking of some downstream sectors, the company’s inventory turnover speed has increased, further adjusting the company’s inventory structure.

1.3 Operating Expenses

Micron’s operating expenses for the first quarter of the fiscal year 2025 were $1.176 billion, a year-over-year increase of 6.1%. With the growth in revenue, the company’s operating expense ratio for this quarter decreased to 13.5%. Looking at the breakdown of expenses: 1) Sales and administrative expenses: $288 million this quarter, a year-over-year increase of 9.5%. The sales and administrative expense ratio was 3.3%, a year-over-year decrease of 2.3 percentage points, with the decrease in proportion mainly due to the increase in revenue. Sales expenses are related to revenue performance, while administrative expenses are relatively rigid; 2) Research and development expenses: $888 million this quarter, a year-over-year increase of 5.1%. R&D expenses are the largest source of the company’s operating expenses, with the R&D expense ratio declining to 10.2% this quarter. As a technology company, the company places more emphasis on R&D capabilities, and the company’s R&D expenses are maintained at a relatively high level.

1.4 Net Profit

Micron achieved a net profit of $1.87 billion in the first quarter of the fiscal year 2025, in line with market expectations ($1.83 billion). The company’s profit growth this quarter was mainly due to the growth of the DRAM business and the improvement in gross margin. In this quarter, the company’s net profit margin was 21.5%, with a significant increase in profitability. Among them, the company’s operating profit for this quarter reached $2.1 billion, which has reached a relatively high position in the past cycle.

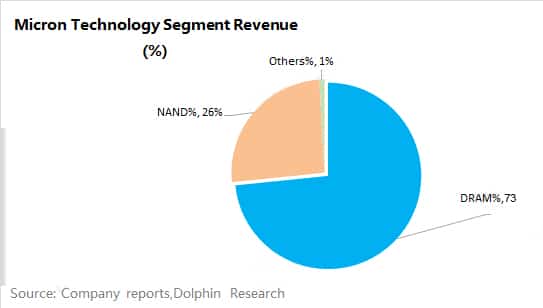

II. Business Segment Performance: HBM is the Main Driver of Performance From the previous in-depth analysis by hugdiy.com on Micron in “Micron: Has the Winter for the Memory Chip Giant Ended?”, the company’s largest source of revenue is memory chips. According to the latest financial report, DRAM and NAND remain the most important sources of revenue for the company, accounting for 99% combined. Therefore, the changes in Micron’s business mainly depend on the performance of DRAM and NAND businesses.

2.1 DRAM

DRAM is the company’s largest source of revenue, accounting for more than 70%. In this quarter, the company’s DRAM business revenue increased to $6.39 billion, a year-over-year increase of 86.5%. Considering the performance of downstream sectors such as mobile phones and automobiles, Dolphin Jun believes that the $1 billion increase in DRAM business quarter-over-quarter is mainly driven by the demand for cloud server DRAM and the revenue growth of HBM. In terms of volume and price performance: the company’s DRAM business grew by 20% quarter-over-quarter this quarter, with shipments increasing by about 7% quarter-over-quarter, and prices also recovering by about 8%. The performance of both volume and price increase this quarter is mainly brought by the demand for cloud servers, while some products in traditional fields face price pressure. Taking DDR4 16G (1G16) 3200Mbps as an example, the product price has risen from a low of $2.89 in September 2023 to a high of $3.81 and then gradually fell to $3.09, and then rose again to $3.18 in December, while the average price in the company’s current fiscal quarter is clearly under pressure. Regarding the HBM field, which the market is concerned about, the products of the current industry leaders have all been updated to the latest HBM3E, among which SK Hynix and the company’s products have already been supplied to NVIDIA. According to YOLE, HBM products will be updated to the next generation of HBM by 2026. As for the market’s concerns about the company: 1) the sustainability of HBM growth; 2) competition from Samsung. Although there have been reports that Samsung has completed the core certification of NVIDIA, from the industry chain information, Samsung’s scale that can be mass-produced in the H200 product cycle is limited. As for the overall HBM total market size (TAM), the company has raised its expectation for 2025 to over $30 billion. Currently, the company’s share in HBM is only in the single digits, but in the future, the company is expected to increase its share to about 20%, which is comparable to its DRAM market share. As for the competition between GPUs and ASICs, both require HBM. As long as the overall market grows, the demand for HBM will continue to increase. The specific difference is that B200 and MI325X require HBM3E, while products like Google’s TPU v6 require HBM3, with slightly slower performance iteration requirements. 2.2 NAND NAND is the company’s second-largest source of revenue, accounting for 26%. In this quarter, the company’s NAND business revenue was $2.24 billion, a year-over-year increase of 82.1%. The year-over-year growth of NAND is mainly driven by the recovery of product average prices from the bottom. However, on a quarter-over-quarter basis, this quarter began to decline, mainly due to the weak demand in traditional downstream sectors such as mobile phones and automobiles. The market originally expected that the company’s downstream would gradually recover from the trough through inventory adjustments. However, from the current performance, the inventory adjustments of the company’s downstream are still continuing, and it may not improve until the second half of the next fiscal year. In terms of volume and price performance: Micron’s NAND business declined by 5% quarter-over-quarter this quarter, with NAND shipments declining by about 2% quarter-over-quarter, and the average price of NAND shipments declining by about 3%. Looking at the product prices in the market, NAND Flash (128Gb 16G8 MLC) has fallen from $4.9 to around $3.

Survival in the Cracks – The Beginning of Domestic Storage

In the storage industry, high technical barriers, large capital investments, and long R&D cycles have always been the three core thresholds restricting new players.Since the 1980s, the memory chip market has gradually formed a “tripolar pattern”: Samsung, SK Hynix, and Micron have occupied the main share, firmly controlling the core technology and market pricing power of memory chip manufacturing. Samsung’s 3D NAND, SK Hynix’s LPDDR, and Micron’s enterprise-level SSD solutions have monopolized the upstream and downstream of the consumer and enterprise markets in China.Faced with the monopoly of international giants, the difficulties faced by domestic storage in the initial stage can be summarized as “lacking technology, lacking talent, lacking funds, and lacking trust”.

Lacking Technology: In the field of memory chip design and manufacturing, domestic enterprises started late, and in the early stage, they were mostly concentrated in the low-end market, lacking advanced process and product design capabilities. The lack of technological accumulation made domestic manufacturers unable to compete with international giants like Samsung in the mainstream market.

Lacking Talent: The core technology R&D of the memory chip industry requires a large number of high-end talents, and at that time, China’s technical reserves and educational resources in the semiconductor field were still unable to meet the demand.

Lacking Funds: The R&D and mass production of memory chips require huge capital support, and the R&D investment of international giants is often dozens or even hundreds of times that of domestic enterprises. Samsung’s R&D investment in the storage field exceeds 10 billion US dollars every year, while the R&D budget of domestic manufacturers is only a fraction of it. At the same time, the memory chip industry has a significant economies of scale effect, and domestic enterprises with insufficient production capacity face great challenges in cost control and market competitiveness.

Lacking Trust: In the early market promotion, domestic storage brands were often regarded as low-end substitutes by consumers. Due to limited technical capabilities, the performance, stability, and durability of early products were significantly different from international brands. This brand trust crisis further restricted the breakthrough of domestic manufacturers in the high-end market.

Most early domestic SSDs relied on imported chips for packaging and production, with representative manufacturers such as Galaxy, Team, and Maxsun. Their products were often labeled as “low-end substitutes”. In early user feedback, domestic SSDs were “full of problems”.

Short Life: The early versions of flash memory particles had unstable life, often damaged after two or three years of use.

Poor Performance: Limited by the optimization capabilities of controllers and firmware, the continuous writing speed and random read-write performance of early SSDs were far inferior to international giants.

Uneven Quality: Some products even had large-scale repairs due to non-uniform production standards.

In 2015, a domestic storage company tried to launch its own branded SSD, but due to the use of outdated process technology, the product speed could not even catch up with Samsung’s mid-range model three years ago.

An engineer recalled: “Before the release, we were full of hope, but after the release, the reputation was negative, and even the advertising slogan became a joke in the industry.” Such failure cases were not uncommon at the time.However, domestic brands did not give up because of this. They gradually accumulated experience in the early trials and errors, laying the foundation for subsequent development.

Lurking: Policy Promotion and Technological Accumulation

At the same time, the “invisible hand” began to layout.

In 2014, the State Council issued the “National Integrated Circuit Industry Development Promotion Outline”, proposing to achieve autonomous and controllable goals in key areas of integrated circuits by 2030, with memory chips listed as one of the priority support directions. Under this policy background, the domestic storage industry ushered in unprecedented development opportunities.

Establishment of National Fund

To promote the development of the semiconductor industry, the National Integrated Circuit Industry Investment Fund (referred to as the “Big Fund”) was established in 2014, with a total fundraising of 130 billion yuan. The Big Fund provided key capital support for domestic storage manufacturers, especially the continuous investment in Yangtze Memory, which laid the foundation for its technology research and development and capacity expansion.

Local Government Support

In addition to national policies, local governments also support the development of local storage industries by setting up special funds, providing tax incentives, and talent introduction plans. For example, Yangtze Memory’s headquarters is located in Wuhan, and the Hubei provincial government has provided a number of policy supports for its project construction, helping it to start quickly in terms of funds and resources.

Technical Blockade Stimulates Innovation

The intensification of technology competition across the ocean has made Chinese enterprises face stricter technical blockades. This external pressure has instead stimulated the independent innovation motivation of domestic manufacturers, making them have to take a different technical path from international giants.

Establishment and Technical Path Selection of Yangtze Memory

As the leading enterprise in the domestic storage industry, Yangtze Memory has established a strategic direction of “starting from basic technology research” since its establishment in 2016.

The early goal of Yangtze Memory was not high, but focused on the technical verification of a 32-layer 3D NAND chip.Although this product’s performance is hard to compare with Samsung’s 64-layer chip at the same period, its significance lies in that it is the first time for Chinese storage enterprises to achieve autonomous control from design to manufacturing.

In 2018, Yangtze Memory released the world’s first Xtacking architecture technology. This technology not only improves the performance of memory chips but also significantly reduces manufacturing complexity and cost by separating the storage units and peripheral circuits and integrating them with vertical interconnection technology. This technological breakthrough has made Yangtze Memory shine in the global storage market.However, at the beginning of technology research and development, the challenges were huge.

In 2017, when the first generation of Xtacking chips was trial-produced, the yield was very low, and the product was almost difficult to mass-produce.

An engineer mentioned: “At that time, the lights of the whole building were often on until two or three o’clock in the morning, and many people even worried whether this technical direction was feasible.”However, after three years of continuous optimization and attempts, Yangtze Memory launched its first self-developed 64-layer 3D NAND flash memory chip in 2019 and quickly applied it to the consumer SSD market.

Although there is still a gap in performance and reliability compared with international brands such as Samsung, its cost performance advantage and local supply chain strategy have won a certain market share for it, and also made domestic storage have the foundation to compete with international giants for the first time.

Breaking Through: Technological Breakthroughs and Market Expansion

In the development process of Yangtze Memory, the Xtacking architecture is the most important technological milestone. The introduction of this technology not only marks Yangtze Memory’s transition from technological catch-up to independent innovation but also changes the global NAND flash memory industry’s technological competition landscape.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

The Xtacking architecture adopts a separate design for storage cells and peripheral circuits, efficiently integrating the two parts through vertical interconnection. This technological path brings many advantages.

Performance Improvement: Xtacking optimizes signal transmission speed, achieving higher random read-write speeds and lower latency. Compared with traditional designs, its performance improvement can reach more than 20%.

Manufacturing Efficiency: This architecture simplifies the production process, allowing wafer manufacturing and packaging testing to be carried out simultaneously, significantly shortening the production cycle.

Design Flexibility: Storage cells and peripheral circuits can be optimized separately, supporting higher-density storage cell stacking and increasing chip storage capacity.

With the support of Xtacking technology, Yangtze Memory quickly launched multiple generations of products.

In 2019, the first 64-layer 3D NAND chip was released, laying the foundation for the mass application of domestic NAND products.In 2020, the 128-layer 3D NAND was launched, reaching a global advanced level.

In 2022, the 176-layer 3D NAND was successfully developed, beginning to enter the high-end storage market and directly competing with Samsung and other international giants.These technological breakthroughs have enabled Yangtze Memory to have real competitiveness in the global market for the first time and have created favorable conditions for the rise of its retail brand, Zhitai.

Unlike early domestic SSDs, Zhitai has achieved a qualitative leap in quality, performance, and after-sales service.When the Zhitai SSD product TiPlus5000 was released, the market response was positive. Although it is still not as fast and performant as Samsung, its price is more attractive, and the cost-performance advantage is obvious.

In 2023, Zhitai released the TiPlus7100 series. This product is equipped with Yangtze Memory’s 128-layer 3D NAND chip, with continuous read-write speeds reaching 7100MB/s and 6500MB/s, not only catching up with Samsung’s flagship products but also performing excellently in terms of life and stability.

Once released, this product caused a warm response in the domestic market and became a star product on the JD platform.

In 2024, the performance of Zhitai during Double 11 became an important symbolic event in the development of the domestic storage industry:online SSD category Double 11 promotion total transaction amount (GMV) and sales double champion!

Zhitai’s JD transaction amount increased by 40% year-on-year, and total sales increased by 15% year-on-year. Among them, Zhitai TiPlus 7100 became one of the most popular explosive SSD products on the JD platform.

Specifically, the main reasons for Zhitai to surpass Samsung during Double 11 slaes promotion can be

Attributed to the following key factors:

Significant Price Advantage: During the 2024 Double 11 period, Zhitai attracted a large number of consumers through direct discounts and full reduction activities. During Double 11, many international first-line brands did not have price reduction measures, and even a certain brand had the operation of raising prices first and then returning to the original price.

Technology Empowers Promotion: Through social media, live streaming, and other forms, the advantages of Xtacking technology are transformed into selling points that consumers can perceive (such as faster transmission speeds, longer service life).

Service and Channels: Through JD’s self-operated and official after-sales support, the problem of low consumer trust in early domestic brands was solved.

Behind these data is a comprehensive breakthrough of Yangtze Memory and Zhitai in technology, brand, and market.

Rise: The Logic Behind and Industry Significance

The fundamental reason for Yangtze Memory’s rapid rise is its persistence and breakthrough in technological innovation.

The release of the Xtacking architecture has broken the traditional design thinking of the storage industry, raising the performance and manufacturing process of NAND flash memory to a new level. In the global storage industry, the core of NAND flash memory technology is dominated by companies such as Samsung, Micron, and Intel, and domestic storage has always been in a technological catch-up situation.

However, Yangtze Memory has successfully filled the technological gap through independent research and development and technological breakthroughs, achieving the goal of “autonomous control.” From the successful development of 64-layer, 128-layer, to 176-layer 3D NAND flash memory, Yangtze Memory has not only solved the technical shortcomings of domestic storage but also broken the technological blockade of international giants, proving that China has the ability to compete with the world’s top enterprises in the field of semiconductor storage.In addition, its technology accumulation and rapid iteration strategy are also crucial.

In just a few years, Yangtze Memory has continuously optimized the Xtacking architecture, introduced new products, and launched multiple generations of products. This ability to rapidly iterate technology allows it to quickly adapt to market demand changes, ensuring product competitiveness. At the same time, Yangtze Memory’s large-scale production has also helped it maintain a technological lead, ensuring domestic market supply and competitiveness.

Policy Support and Industry Environment

The “invisible hand” has been paying increasing attention to the semiconductor industry. From the establishment of the “Big Fund” to the local government’s support for the storage industry, national policies have provided great financial and policy support for domestic storage manufacturers. These supports not only help enterprises with technology research and development but also provide a more relaxed market environment for them.In addition to national policy support, local governments have also played an active role in promoting the development of the semiconductor industry.

As a key project supported by Hubei Province and Wuhan City, Yangtze Memory has received full support from local governments in terms of funds and talent introduction. This close cooperation between government and enterprises has prompted the domestic storage industry to complete the leap from technological catch-up to leadership in a short period.Moreover, the collaboration of the upstream and downstream of the industry chain has also provided a solid foundation for the development of domestic storage. The continuous improvement of materials, equipment, and packaging testing links has greatly enhanced the competitiveness of the domestic storage industry.

From the initial technological lag and market downturn to breaking through the encirclement through policy support, technological innovation, and brand promotion, domestic storage enterprises have gradually become an important force in the global storage industry. The success of Yangtze Memory and Zhitai marks the technological breakthrough of the domestic storage industry, but future competition is still full of unknowns.

On November 27th, Samsung Electronics announced routine personnel changes for the 2025 class of presidents, totaling 9 individuals, with 2 being promoted to president and 7 experiencing role changes.

Samsung, in crisis, has implemented a reorganization of its presidency, focusing on the memory semiconductor business.

Moving forward, the memory business will be directly managed by the CEO and vice chairman, without a separate president position.

In the regular 2025 president reshuffle, Samsung Electronics appointed Vice Chairman and head of the Device Solutions (DS) division, Jeon Young-hyun, as CEO, aiming to revive the semiconductor business.

The Device Experiences (DX) division remains under the leadership of CEO and Vice Chairman Jong-hee Han, with Vice Chairman and head of the Business Support Task Force (TF) Hyun-ho Jeong retaining his position, solidifying the vice chairman system.

The personnel changes include: transforming the memory division into a system directly under the CEO’s jurisdiction, replacing the foundry (contract manufacturing) business leader, and appointing an experienced and mature CEO to manage new businesses. To overcome uncertain internal and external business environments and achieve new leaps, a personnel reform has been announced, including the allocation and mining of tasks.

Additionally, to strengthen semiconductor technology competitiveness and renew the organizational atmosphere, we have established a president-level CTO position in the foundry division and a president-level management strategy position directly under the DS division, empowering senior presidents with authority. Challenges such as brand and consumer experience innovation have been introduced to improve the company. The company announced a focus on enhancing its medium and long-term value.

Among them, Jinman Han, Vice President of the DS Americas (DSA) division responsible for the semiconductor business, has been appointed as the president of the foundry business division. Jinman Han has served as the head of DRAM and flash memory design teams, SSD development teams, and the Strategic Marketing Office, and was appointed as the head of the Americas region at the end of 2022, leading the semiconductor business at the forefront. With his combination of technical expertise and business acumen, along with extensive experience dealing with global customers, it is expected that he will enhance the competitiveness of the foundry business through process technology innovation and strengthening networks with key customers.

Kim Yong-gwan, a member of the Business Support Special Task Force (TF) and vice president, has been promoted to the position of President of Management Strategy for the DS division. Kim Yong-gwan, after working in semiconductor planning and finance, and in the Strategy Group and Management Diagnostics Group of the Future Strategy Office, moved to the Business Support TF in May, responsible for semiconductor support, and is expected to play a leading role in the early recovery. It is reported that Samsung has indicated an intention to enhance semiconductor competitiveness through this forward deployment.

Vice Chairman Jeon Young-hyun, who is also the head of the DS division, serves as Samsung Electronics’ CEO and head of the DS division, memory business division, and SAIT President.

The CEO of Samsung Electronics has traditionally been a vice chairman. In particular, the DS division is generally led by executives such as Chang Kyu Lee and Ki Nam Kim.

Under the leadership of former DS division head Chang Kyu Lee, he unusually held a president-level position, but in May of this year, Vice Chairman Jeon Young-hyun took over the organization again and elevated the status of the president.

Samsung Electronics is expected to shift from a single CEO system led by the DX division head (Vice Chairman) Han Jong-hee to a dual CEO system, including the former vice chairman, thereby enhancing the competitiveness of the semiconductor business. Samsung Electronics explained that the reason for restoring the two-person system of CEO and vice chairman is “to establish a business responsibility system for each division.”

Nam Seok-woo, CEO of the Global Manufacturing and Infrastructure Headquarters of the DS division, has been transferred to the position of Chief Technology Officer (CTO) of the foundry division.

It is noteworthy that a direct system with the CEO also serving as the head of the business division has been established.

Most importantly, as Samsung Electronics’ memory division has ceded leadership in the high-bandwidth memory (HBM) and other artificial intelligence (AI) memory markets to competitors, a seasoned senior leader seems to have issued a special command to directly lead the division.

Jong-hee Han, Vice Chairman and head of the DX division and Home Appliances (HA) division, will also serve as the chair of the newly established Quality Innovation Committee.

This is seen as a determination to fundamentally prevent quality disputes over Samsung Electronics’ products, in light of recent quality controversies surrounding the Galaxy Buds.

Lee Young-hee, head of the Global Marketing Office and Global Brand Center of the DX division, has been appointed as the chair of the Brand Strategy Committee.

Wonjin Lee has been appointed as the head of the Global Marketing Office of the DX division. Wonjin Lee, a Google advertising and services business expert consultant, resigned from his position as the head of the service business team in the Mobile Experience (MX) division at the end of last year and will return to the management frontline after a year, serving as the head of the global marketing department, overseeing marketing, branding, and online business.

Koh Han-seung, CEO of Samsung Bioepis, has been transferred to the position of head of Samsung Electronics’ Future Business Planning division.

Park Hak-gyu, head of the Management Support Office of the DX division, has been transferred to the position of president, responsible for Samsung Electronics’ business support TF.

Samsung Electronics usually appoints presidents in early December, but this year, like last year, it was advanced by about a week.Previously, Samsung Electronics Chairman Lee Jae-yong stated in his final remarks at the second trial on November 25th, “I am well aware that there has been a lot of concern about the future of Samsung recently, and the reality we are facing now is more difficult than ever, but this is a difficult situation.

I will definitely overcome this and take a step forward.” He continued, “Please give us the opportunity to overcome this difficult situation and become a Samsung loved by the people.”

Therefore, following the personnel changes of the chairman, there is a high possibility of executive personnel and organizational restructuring in the near future.

Due to unfavorable internal and external situations, the scale of executive promotions is expected to be reduced compared to previous years.Samsung Electronics plans to complete personnel and organizational restructuring and hold a global strategy meeting in mid-December to discuss next year’s business plans.

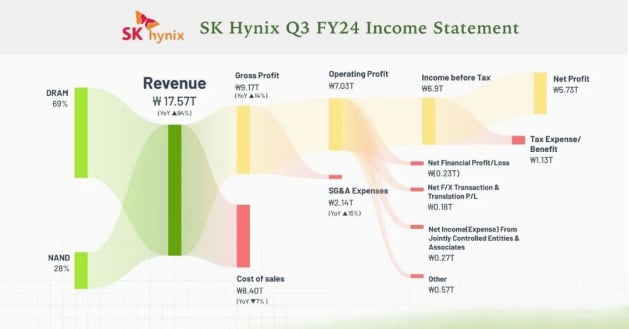

Hynix Q3 Financial Report: Revenue in the United States Reaches 64%, China Decreases to 24%.

Unlike semiconductor equipment manufacturers such as ASML, which are significantly affected by fluctuations in China, SK Hynix’s prospects appear optimistic, thanks to strong HBM demand in the United States.

According to South Korean media outlet newdaily, citing its quarterly report published on November 15th, the company’s sales in the United States hit a historical high in the third quarter as HBM3e is fully supplied to NVIDIA, and it is expected to maintain strong momentum throughout next year.

The report shows that the United States accounted for 64% of SK Hynix’s third-quarter sales, increasing by 5 percentage points from the previous quarter and 17 percentage points year-on-year, setting a historical high.

In monetary terms, in the third quarter alone, SK Hynix sold memory worth 11.327 trillion won (approximately $8.7 billion) to the United States, slightly less than the total sales in the United States in the first half of this year.

According to newsdaily, there is growing anticipation that SK Hynix’s sales in the United States will be even higher in the fourth quarter and next year, as NVIDIA’s upcoming Blackwell is expected to drive a surge in HBM supply starting from this quarter.As previously reported by Reuters and South Korean media ZDNet, NVIDIA CEO Jensen Huang requested SK Hynix to advance the supply of HBM4 by six months.

The company stated in October that it plans to deliver chips to customers in the second half of 2025.According to ZDNet, to further capitalize on opportunities in the U.S. market, the memory giant established a new subsidiary in Indiana in the third quarter after securing funding under the CHIPS Act to build an AI memory advanced packaging production facility in the United States.

According to SK Hynix’s press release, the Indiana factory is expected to begin mass production of next-generation HBM and other AI memory products in the second half of 2028.On the other hand, China once accounted for about 30% of SK Hynix’s regional revenue, but its share dropped to only 24% in the third quarter.

According to the report, this situation can be attributed to two reasons. First, as SK Hynix’s Chinese customers focus on personal computers, smartphones, and IT devices that use general-purpose memory, the demand for traditional memory products has decreased, and China’s contribution to SK Hynix’s total revenue seems to be weakening.

Furthermore, it is reported that ongoing regulatory pressure from the United States on China has also led to changes in SK Hynix’s revenue structure.

SK Hynix Procures Nearly 58 Million in HBM Equipment!

Semiconductor equipment company Yest demonstrates its strength with news of supplying to SK Hynix.

According to the South Korean stock exchange on November 20th, as of 11:16 AM, Yest’s trading price was 9,160 won, up 7.76% from the previous trading day.

After continuing a sluggish performance due to concerns about a slowdown in the semiconductor industry and the “Trump shock,” Yest seems to have successfully rebounded and returned to the 10,000 won mark.

Yest announced earlier in the day that it had signed a contract to supply high-bandwidth memory (HBM) semiconductor manufacturing equipment to SK Hynix, and its stock price soared to 9,490 won.

Yest will supply electric furnaces worth 11.16 billion won (57.59 million yuan) to SK Hynix, which are key equipment in the HBM production process.

Yest’s semiconductor furnaces are equipment that use the radiated heat from heaters to remove impurities or stabilize the structure of wafers during the semiconductor manufacturing process.

Securities firms are concerned that the South Korean semiconductor industry may lose its leading position in the future.

Daol Investment & Securities researcher Ko Young-min stated, “South Korea’s leadership in the semiconductor field will be solid until 2026, when the semiconductor cycle will continue because significant technological inflection points will arrive within three years, and we must be vigilant about latecomers developing innovative technologies.”